Cheque Bounce Case Under Section 138: Your Complete Legal Guide

Understand the legal process, penalties, timelines, and defenses involved in cheque bounce cases under Section 138 of the Negotiable Instruments Act

Receiving a bounced cheque can be frustrating and financially damaging. But Indian law provides strong remedies for victims of cheque dishonour through Section of the Negotiable Instruments Act, . This comprehensive guide explains everything you need to know about filing a cheque bounce case, including the critical -day notice requirement, the legal procedure, potential penalties, and how to maximize your chances of recovering your money.

Understanding Section : The Legal Framework

Section of the Negotiable Instruments Act makes the dishonour of a cheque a criminal offense punishable with imprisonment up to two years, a fine up to twice the cheque amount, or both. This provision was introduced to enhance the credibility of cheques as a mode of payment and to protect payees from dishonest drawers.

Key Elements of Section

For a cheque bounce case to be valid under Section , several conditions must be met. The cheque must have been issued for the discharge of a legally enforceable debt or liability. The cheque must have been presented to the bank within its validity period ( months from the date on the cheque or the period mentioned on the cheque). The cheque must have been returned unpaid due to insufficient funds or because it exceeds the arrangement with the bank. The payee must have sent a legal notice within days of receiving the "cheque returned" memo. The drawer must have failed to make payment within days of receiving the notice.

The Critical -Day Rule

This is the most important deadline in any cheque bounce case. After your bank returns the cheque with a memo stating the reason for dishonour (typically "insufficient funds" or "exceeds arrangement"), you have exactly days to send a legal notice to the cheque issuer demanding payment.

Why the -Day Deadline Matters

Missing this deadline is fatal to your case. If you don't send the notice within days, you lose your right to file a criminal complaint under Section . You may still have civil remedies, but the powerful criminal prosecution option — which often motivates quick payment — will no longer be available.

Calculating the Days

The -day period starts from the date you receive the "cheque returned" memo from your bank, not from the date the cheque was presented or the date it was returned by the drawer's bank. Keep the bank memo safely as it's crucial evidence.

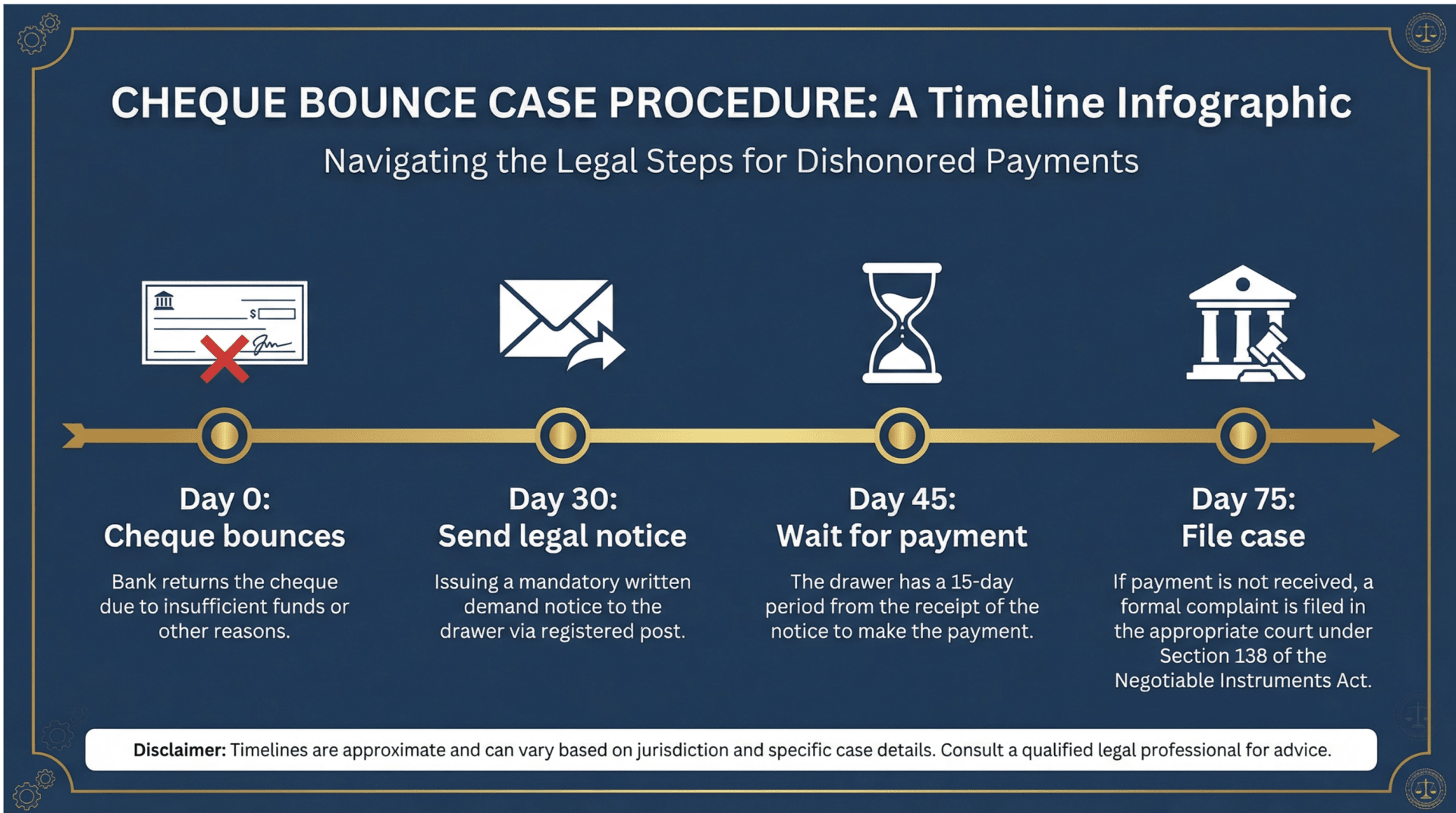

Step-by-Step Procedure for Cheque Bounce Cases

Step 1: Receive the Cheque Return Memo

When a cheque bounces, your bank will provide a memo stating the reason for dishonour. Common reasons include "insufficient funds," "exceeds arrangement," "account closed," "signature mismatch," "payment stopped by drawer," and "refer to drawer."

Important: Only certain reasons qualify for Section prosecution. "Insufficient funds" and "exceeds arrangement" are the primary grounds. Other reasons like "signature mismatch" may require different legal approaches.

Step 2: Send Legal Notice Within Days

Within days of receiving the return memo, send a legal notice to the drawer demanding payment of the cheque amount. The notice should clearly state the cheque details (number, date, amount, bank), the reason for dishonour, a demand for payment within days, and a warning that criminal proceedings will be initiated if payment is not made.

The notice must be sent via Registered Post with Acknowledgment Due (RPAD) to create proof of delivery.

Step 3: Wait Days for Payment

After the drawer receives your notice, they have days to make the payment. If they pay within this period, the matter is resolved and you cannot file a criminal case.

Step 4: File Criminal Complaint Within Days

If the drawer fails to pay within days of receiving the notice, you have days to file a criminal complaint in the appropriate Magistrate's court. This -day period starts from the date the -day notice period expires.

Step 5: Court Proceedings

Once the complaint is filed, the court will examine the complaint and evidence, issue summons to the accused if a prima facie case exists, conduct trial proceedings, and deliver judgment.

Penalties for Cheque Bounce

Under Section , the penalties for cheque dishonour can be severe. The drawer may face imprisonment for a term up to two years, a fine up to twice the amount of the cheque, or both imprisonment and fine. Additionally, under Section of the CrPC, the court can order the accused to pay compensation to the complainant.

Defenses Available to the Accused

The drawer of a bounced cheque may raise several defenses. These include claiming the cheque was not issued for a legally enforceable debt, arguing the cheque was given as security and not for payment, asserting the notice was not received or was defective, claiming the complaint was filed beyond the limitation period, or proving payment was made within the -day notice period.

Recent Legal Developments

Supreme Court Guidelines

Recent Supreme Court judgments have clarified several aspects of Section cases. In Dashrath Rupsingh Rathod v. State of Maharashtra (), the court held that the complaint must be filed where the cheque was delivered for collection. The Expeditious Trial guidelines mandate that cheque bounce cases should be disposed of within months.

Negotiable Instruments (Amendment) Act

The amendment introduced provisions for interim compensation. Courts can now direct the drawer to pay interim compensation of up to % of the cheque amount, which must be paid within days. This provides quicker relief to complainants.

Practical Tips for Cheque Bounce Cases

For the Complainant (Payee)

Act quickly — the -day notice deadline is strict and missing it is fatal. Preserve all documents including the original cheque, bank memo, notice copy, and postal receipts. Use RPAD for sending the notice to ensure proof of delivery. Consult a lawyer before sending the notice to ensure it's properly drafted. Be prepared for a long process — despite expeditious trial guidelines, cases can take - years.

For the Accused (Drawer)

Respond to the notice within days if you have a genuine defense. Make payment if the debt is legitimate to avoid criminal prosecution. Consult a lawyer immediately upon receiving a notice. Don't ignore the notice or court summons — it will only make things worse.

Cheque Bounce vs. Civil Recovery

While Section provides criminal remedies, you also have civil options for recovering money. Civil suits can be filed for larger amounts without the strict timelines of Section . However, criminal cases under Section are often more effective because the threat of imprisonment motivates quicker settlement, criminal courts are generally faster than civil courts, and the accused cannot easily delay proceedings.

Many complainants file both criminal and civil cases simultaneously to maximize pressure on the defaulter.

How Kaanuni Paramarsh Can Help

Time is critical in cheque bounce cases. With only days to send the legal notice, you need fast, professional service. Kaanuni Paramarsh offers AI-drafted legal notices for cheque bounce cases starting at ₹999 with lawyer verification to ensure legal validity, -hour delivery to meet your deadline, RPAD dispatch with tracking, and follow-up guidance for next steps.

Don't let the -day deadline pass. Send your cheque bounce notice now and protect your right to criminal prosecution.

Frequently Asked Questions

Q: Can I file a case if the cheque bounced due to "signature mismatch"?

Section specifically covers dishonour due to insufficient funds or exceeding arrangement. For signature mismatch, you may need to pursue civil remedies or investigate whether the signature issue was genuine or an attempt to avoid payment.

Q: What if the drawer has closed their account?

If the account was closed after issuing the cheque, Section may still apply. However, if the account was already closed when the cheque was issued, it may indicate fraud, which requires different legal action.

Q: Can I file multiple cases for multiple bounced cheques?

Yes, you can file separate cases for each bounced cheque. However, if multiple cheques were issued for the same transaction, courts may consolidate the cases.

Q: What happens if the accused doesn't appear in court?

The court can issue a bailable warrant, and if the accused still doesn't appear, a non bailable warrant. Continued absence can result in ex-parte proceedings.

Conclusion

Cheque bounce cases under Section provide a powerful remedy for victims of dishonoured cheques. However, the strict timelines — especially the -day notice requirement — mean you must act quickly and correctly. With proper legal guidance and timely action, you can recover your money and hold the defaulter accountable.